Treasury Essentials

June 2026

Welcome to Treasury Essentials, our bi-annual insight into topical issues of relevance to finance and treasury teams.

This month, we focus on the debt capital markets, which have been very active during the first half of 2026. Investor appetite appears to remain strong, but many would-be issuers will have experienced the sensitivity of the market to the economic and geopolitical landscape. Shifts in inflation expectations, interest rate trajectories and the news cycle generally mean issuers and their advisers are acutely aware of the need to approach funding options strategically. Treasurers are taking steps to ensure they are ready to move swiftly to take advantage of favourable conditions as they arise – and with a “plan B” in hand, if they do not.

We kick off this edition with a closer look at the bond market backdrop in Europe, before turning to more technical matters, including a recap of the recent reforms to both the UK and EU prospectus regimes and an overview of the implications of the forthcoming reform to the Retail Prices Index (RPI) for index-linked securities. We also revisit the topic of convertibles, which are currently experiencing a resurgence in Europe, but also globally.

We hope you enjoy our “bond market special”. If you would like to explore any of the topics covered in more detail, or if you have any thoughts or feedback on this or previous editions, please get in touch with either of us, or any of the lawyers listed at the end of this publication.

If any of your colleagues or contacts would like to receive this publication, please click here. You can find previous editions of Treasury Essentials here.

Resilience and opportunity - 2026 YTD in the bond markets

The European debt capital markets have remained open and broadly resilient in the face of persistent macroeconomic and geopolitical uncertainty since the start of the year. Investment grade issuance has been strong overall, subject to intermittent disruption following the outbreak of the Iran conflict. The high yield market has been more sporadic, experiencing a pronounced pause towards the end of Q1, but has rebounded since.

Across both markets, investor demand has been an important stabilising force, with healthy cash balances and appetite for high-quality credit supporting well-covered orderbooks. For high grade issuers and popular high yield names, the markets remain open subject to execution windows, making the ability to move quickly critical to accessing liquidity on the most attractive terms.

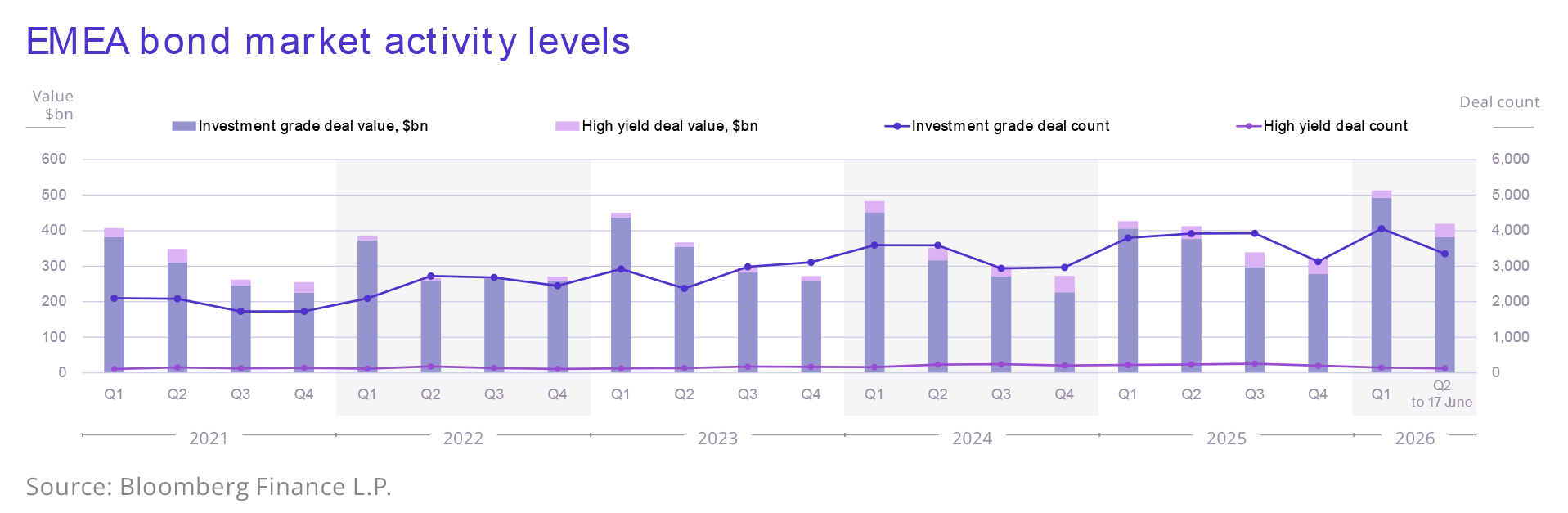

EMEA bond market activity levels

Investment grade supply remains strong

The investment grade market had a successful start to the year. Q1 global volumes and deal counts reached their highest quarterly levels in five years. Supply has remained healthy through Q2, supported by a number of “Reverse Yankee” transactions. H1 has also seen elevated issuance levels of corporate hybrids, alongside a marked flow of convertibles, a five-year high in terms of volumes.

Reverse Yankee issuance - where US corporates issue bonds in non-US currencies like euro and sterling, principally to diversify their funding base and take advantage of pricing differentials - has been a notable feature of the 2026 market, with reports of borrowing by US corporates in Europe having reached more than €60 billion by early June. This figure includes some very large deals: Amazon’s record €14.5 billion eight-tranche deal in March and Alphabet’s €9 billion six-tranche issuance in May. The appeal is economic, driven in large part by the continuing favourable movement of the USD against both EUR and GPB.

Hybrids - subordinated instruments which sit between debt and equity for accounting and ratings purposes - tend to come from issuers who want to protect their ratings and meet their M&A or capex funding requirements during periods of growth. Interest in hybrids is traditionally focused in the utilities and energy sectors, but this year the European market has seen issuance from other sectors including manufacturers and industrials. The make-up of, and drivers for, the increase in convertibles are discussed in detail later in this edition.

High yield regains momentum after March disruption

The European high yield market began the year strongly, with January’s supply of €13.3 billion setting a new record for the month, according to PitchBook. Activity effectively ground to a halt for much of March following the outbreak of the Middle East conflict and the resulting shift in expectations around inflation and interest rates, underscoring the greater sensitivity of lower-rated issuance to bouts of volatility.

Since then, high yield has regained momentum, as buyers started to look through ongoing geopolitical uncertainty. More supportive conditions, including a contraction in average spreads, have encouraged a broader range of borrowers to come to market, including issuers with more challenging credit stories or exposure to less favoured sectors. According to Octus, European high yield issuance had reached approximately €58.9 billion by the end of May, already exceeding full-year 2022 and 2023 volumes and tracking broadly in line with 2025’s record pace.

Beneath the headline numbers, refinancing continues to dominate supply, accounting for around 67% of deal count according to Octus (broadly consistent with the 2025 pattern). A slight increase in dividend recapitalisations at the same time suggests a degree of renewed sponsor confidence.

Readiness and optionality remain key

For corporate issuers, the 2026 bond market might be characterised as constructive yet unsettled. Access may not be uniform across sectors, ratings categories or structures, but investor demand remains strong. The obvious influences on market activity - the trajectory of interest rates, renewed inflation risk, the sustainability of the re-opening of the Strait of Hormuz – persist, but that persistence appears to mean market participants are becoming more adept at navigation. Some recent reports suggest that banks are changing their pre-marketing strategies for high yield issuance, to shorten the time to market, for example.

More generally, this backdrop underscores the continuing importance of being agile and well-prepared. Funding plans are being made further in advance, with careful attention to the interplay between loans and bonds. Both debut and seasoned issuers are advised to ensure that documentation, consents and internal authorities are kept on the stocks, and regularly refreshed, so that they are ready to move when market conditions are favourable. Maintaining optionality across funding sources will also be important in ensuring treasury teams are able to respond quickly to changing pricing dynamics and secure funding on the most attractive terms available.

Prospectus regime reforms in focus - what’s changed in the UK and EU

The UK and EU prospectus regimes have undergone a series of reforms over the last few years, affecting issuers of securities listed on UK and EU regulated markets. While changes in both regimes represent targeted refinements for debt securities, the UK reforms have been structurally more significant. On 19 January 2026, the new UK Public Offers and Admissions to Trading regime (the POATRs) came into force, replacing the UK prospectus rules inherited from the EU. Meanwhile, in the EU, reforms to the EU Prospectus Regulation under the EU Listing Act have been implemented on a staggered timetable, with the latest changes taking effect from 5 June 2026. This article summarises the key points to consider for issuers of debt securities.

The UK Public Offers and Admissions to Trading regime

On 19 January 2026, the new POATRs regime came into force, replacing the UK prospectus regulation-based regime inherited from the EU. The new rules are designed to reduce costs for issuers of admitting securities to trading on UK regulated markets, make capital raising easier and remove barriers to retail participation. Key changes include the following (see our client briefing for further detail):

- a single wholesale-based prospectus disclosure standard now applies for all debt securities (regardless of denomination) and a prospectus summary is no longer required for debt securities;

- there is a new concept of “Plain Vanilla Listed Bonds” (broadly, senior unsecured, plain vanilla, listed bonds). UK listed corporate issuers that issue Plain Vanilla Listed Bonds benefit from certain alleviations and guidance to make retail participation more accessible;

- there are new prospectus disclosure requirements and guidance for green, social, sustainable and sustainability-linked bonds; and

- MTN programme issuers have the option to future incorporate by reference annual and interim financial information into their prospectuses, doing away with the need to supplement for this purpose.

From a practical perspective, London Main Market listed programme issuers approaching annual updates will need to consider the applicable changes, including updates to base prospectus selling restrictions and legends for the new regime.

Plain Vanilla Listed Bonds

The new rules on Plain Vanilla Listed Bonds are likely to be of particular interest to eligible UK corporate issuers, with the London Stock Exchange applying a new "Access Bond" designation to retail eligible bonds (including, but not limited to, Plain Vanilla Listed Bonds) admitted to its Main Market.

A small number of issuers have since included the ability to issue low denomination bonds and related mechanics in their MTN programmes. In addition, the London Stock Exchange Group PLC has gone further by converting three series of its outstanding sterling bonds from £100,000 to £1,000 denominations through a consent solicitation process, qualifying them as Access Bonds available to retail investors in the secondary market. These developments may encourage other issuers to consider low denomination issuance and may, over time, support broader retail investor participation in the UK corporate bond market.

EU Prospectus Regulation reforms under the EU Listing Act

Background

The EU Listing Act, which was published in November 2024 and forms part of the EU’s wider Capital Markets Union project, is a package of reforms designed to make the EU public capital markets more attractive for companies of all sizes. It amends various EU regulations including the EU Prospectus Regulation.

The changes have been implemented on a staggered basis, with some changes having applied when the EU Listing Act came into force in December 2024 and others taking effect up to 18 months later. Further changes to the EU Prospectus Regulation at Level 1 took effect on 5 June 2026. These Level 1 changes are supplemented at Level 2 by the EU PR Amending DR (as defined below).

Latest changes

On 7 May 2026, the European Commission adopted a Delegated Regulation amending Delegated Regulation (EU) 2019/980 (as regards the format, content, scrutiny and approval of the prospectus to be published when securities are offered to the public or admitted to trading on a regulated market), together with related disclosure annexes (the EU PR Amending DR).

The EU PR Amending DR will only enter into force after a scrutiny period by the European Parliament and the Council, creating a timing mismatch. In particular, certain new Level 1 requirements of the EU Prospectus Regulation apply from 5 June 2026, but the detailed Level 2 measures (the EU PR Amending DR) will not yet be in force by that date. To bridge this legislative gap, the European Securities and Markets Authority (ESMA) has recommended that issuers and other stakeholders follow the provisions of the EU PR Amending DR (as adopted on 7 May 2026) when determining the detailed disclosures needed to satisfy the new Level 1 requirements from 5 June 2026, despite the fact that the EU PR Amending DR will not formally be in force by that time.

Key changes for issuers of debt securities are set out below.

New disclosure requirements for ESG Bonds

There are new ESG disclosure requirements for issuers of debt securities advertised as taking into account ESG factors or pursuing ESG objectives (ESG Bonds), requiring additional information to be included in the prospectus in accordance with a new Annex 23 to the EU PR Amending DR (the ESG Annex). The requirements are mostly based on previous ESMA guidance issued in 2023 and include the following:

- for all ESG Bonds, the issuer will be required to include an unambiguous, fact-based explanation in the prospectus to help investors understand the ESG factors taken into account or the ESG objectives pursued by the bonds;

- where an ESG Bond is advertised as aligned with or otherwise adhering to the EU taxonomy, the prospectus must clearly state the minimum percentage of the proceeds which will be allocated to activities aligned with the EU taxonomy;

- where the bonds are aligned with a market standard or label, the prospectus must (i) identify the market standard or label and (ii) include a hyperlink to the disclosures relating to that market standard or label (e.g. an applicable framework);

- for use of proceeds bonds, the prospectus must list the sustainable projects or activities to be financed with the bond proceeds, describe their objectives and how they meet defined sustainability criteria, and disclose any permitted deviations from the intended use of proceeds (with criteria for selecting projects if they aren’t yet identified);

- for sustainability-linked bonds, the prospectus must describe any financial terms (e.g. interest or premium adjustments) that depend on the issuer’s success or failure in meeting specified ESG targets (i.e. the bond’s KPIs and SPTs), including how those adjustments are calculated. The prospectus must also explain the chosen KPIs and SPTs (with their calculation methods) and how they are consistent with the relevant sector-specific science-based targets (where any) and the issuer’s sustainability strategy. In addition, the prospectus must disclose any impact of early amortisation on the sustainability performance of the investment;

- the prospectus must state whether the issuer intends to provide any sustainability-related updates after issuance, and if so, where investors can find that information;

- if the issuer chooses to use any ESG rating assigned to the ESG Bond, the prospectus must include a hyperlink to that rating. The prospectus must also include a hyperlink to any external review or second-party opinion on the ESG Bond (where any); and

- European Green Bonds under the EU Green Bond Standard are not covered by the ESG Annex as well as bonds marketed as environmentally sustainable and sustainability-linked bonds, provided the issuer has chosen to use the voluntary disclosure templates under the EU Green Bond Regulation. In each such case, however, the issuer must incorporate the relevant information from the green bond factsheet or voluntary templates into its prospectus.

Prospectus format and content requirements

The EU PR Amending DR merges and streamlines the previously separate retail and wholesale annexes into a single disclosure framework for debt securities. However, this changes little in practice as the merged annexes still contain differentiated disclosure requirements for wholesale and retail debt (for example, the requirement to produce a summary will continue to apply to retail only).

One key change, however, is that the requirement for audited financial information for standard debt prospectuses has been reduced from two financial years to one financial year, although whether this changes market practice remains to be seen.

The EU PR Amending DR also introduces a mandatory sequence for certain standalone plain vanilla debt prospectuses, based on the order of sections set out in Annex 16 to the EU PR Amending DR. However, base prospectuses under MTN programmes as well as certain drawdown prospectuses are excluded from this requirement.

Grandfathering

Importantly, transitional provisions under the EU Prospectus Regulation (at Level 1) mean prospectuses approved before 5 June 2026 are grandfathered for the remainder of their 12-month validity and so issuers will not need to consider the above changes until their next programme update.

Planning for RPI reform – taking steps ahead of 2030

On 25 November 2020, following a joint consultation, HM Treasury and the UK Statistics Authority announced that the Retail Prices Index (RPI) would be reformed to address perceived shortcomings in the calculation of RPI, by bringing the methods and data sources of the Consumer Prices Index, including owner occupiers’ housing costs, into the calculation of RPI (the RPI Reforms). The then Chancellor of the Exchequer indicated that he would not consent to the implementation of the RPI Reforms prior to 2030, therefore avoiding the need to consider any adjustments to “old style” eight-month lag index-linked gilts. Following a dismissed application for judicial review of the decision to implement the RPI Reforms by the High Court in 2022, the RPI Reforms are now set to come into effect from February 2030.

Unlike for index-linked gilts, the RPI Reforms may expose issuers of, and investors in, RPI-linked securities to the risk of uncertainty in determining the applicable inflating rate after 2030. This will be particularly relevant for financial institutions, pension funds, the utilities sector, the investment arms of insurers and assurers and those in the commercial real estate sector, all of whom have significant exposures to inflation-linked instruments. Experience of similar market developments in the recent past (i.e. IBOR cessations) has shown that addressing this type of issue can be complex and that it is prudent to look ahead to address the upcoming reform.

Futureproofing against RPI reform

The pool of issuers with outstanding RPI-linked securities is reasonably sized and somewhat diverse. With 2030 fast approaching, certain issuers of RPI-linked securities are now beginning to consider the potential impact of the RPI Reforms on their outstanding RPI-linked debt.

We have been closely involved in discussions with clients around RPI Reform, including in relation to potential forward-looking updates to the index-linked terms and conditions of Euro-Medium Term Note (EMTN) programmes, as well as possible retrospective amendments to the terms and conditions of legacy RPI-linked debt in order to reduce reliance on outdated RPI fallback provisions which may no longer be appropriate following implementation of the RPI Reforms.

How will RPI-linked securities be impacted?

Whilst the fallback provisions across RPI-linked debt securities are not uniform and therefore require careful assessment of the precise mechanics, most contain provisions that, upon a fundamental change to RPI, allow a third-party expert to recommend adjustments or a substitute index. However, many of these provisions have become outdated: they offer no scope for pre-emptive action, often bypass any assessment of HM Treasury recommendations on the reference gilt, and in some circumstances this could result in early redemption at indexed par. Such provisions generally rely on the appointment of an expert at a time when, as IBOR cessation demonstrated, willing institutions may be difficult to find. Where an expert can be appointed, the cost may be significant and the basis for its determination is often unclear, creating uncertainty in the market. The fallback provisions and related impact are discussed in further detail in our previous client briefing (see here).

Recent work: United Utilities

In March 2026, United Utilities Water PLC (United Utilities) took proactive steps to amend the terms and conditions of some of its RPI-linked securities to address the forthcoming RPI Reforms.

2022-2023: Early considerations

In November 2022, United Utilities made updates to the fallback provisions for new RPI-linked notes issued under its EMTN programme, including the introduction of a reference gilt-based fallback, aimed at mitigating the risk of redemption at indexed par following RPI reform.

Following this, we advised United Utilities in 2023 on engaging with investors, via the Investment Association, to explore retrospective adoption of these updated fallbacks across its existing RPI-linked notes.

Whilst initial discussions were constructive, they were not conclusive, and United Utilities resolved to pursue further engagement with holders of its RPI-linked debt, either individually or through ad hoc groups, to explore potential amendments.

2026: Amendment of certain legacy RPI-linked instruments

In 2025, United Utilities identified three series of legacy RPI-linked notes issued under its EMTN programme (the Relevant Notes) to be used in a test case for amendment.

United Utilities agreed a set of amendments (the Amendments) to the terms and conditions of the Relevant Notes in order to, amongst other things: (i) revise certain RPI fallback provisions to create greater certainty upon the cessation of RPI, and (ii) adjust the maturity profile of two of the Relevant Notes as part of a broader optimisation of United Utilities’ debt profile and to meet noteholder objectives.

United Utilities agreed the Amendments with 100% of the holders of the Relevant Notes. This enabled the Amendments to be implemented efficiently through a bilateral extraordinary resolution by way of written resolution (in line with the terms and conditions of the Relevant Notes), avoiding the need for a wider consent solicitation process.

We worked closely with the United Utilities treasury team in structuring the transaction and led coordination across key stakeholders, including the trustee and agent. We also advised on listing and regulatory requirements and compliance with ongoing disclosure obligations.

How can we help?

We frequently advise leading UK issuers with RPI-linked debt exposure on all manner of debt capital markets transactions. In recent years, we have supported many issuers in amending their debt programmes and implementing new, compliant standalone documentation to address other similar market developments, including for changes to legal and regulatory regimes. We would welcome the opportunity to discuss with other issuers the practical steps involved in amending the terms of their RPI-linked securities in advance of the RPI Reforms.

Beyond vanilla bonds – convertibles in the spotlight

Convertible bonds are experiencing a global resurgence. In EMEA, $3.73 billion was raised across 11 transactions in Q1 2026 - more than double the $1.69 billion recorded in Q4 2025[1]. In the US, issuance exceeded $120 billion in 2025 - a record - and this year, issuance values had reached $65.4 billion by April 2026[2]. The story is similar in APAC, where 2025 issuance volumes tripled compared to previous years[3].

Convertibles can be a valuable, efficient funding tool for corporates in the right circumstances. Historically a cyclical product, convertibles tend to resurface in volatile markets against a backdrop of higher interest rates - which some might simply describe today as “business as usual”. Could the persistence of these economic markers suggest that convertibles will become a structural - rather than cyclical - feature of the funding landscape?

This article outlines the nature of convertible bonds, the main drivers from the issuer’s perspective, alongside some of the key legal, structural and documentation considerations.

What are convertible bonds?

Convertible bonds are typically fixed rate bonds that contain an option for the bondholder to convert the bond into ordinary shares of the issuer (or an entity closely related to the issuer), during a specified period and at a specified price. The embedded conversion option offers investors the certainty of debt exposure (subject to normal credit considerations) with the potential for equity upside in a single instrument.

The conversion price is set higher than the price at which the shares are trading on issuance. This is why convertible issuance can favour younger companies with high growth potential, as illustrated by the chunk of recent primary issuance, in particular in the US, stemming from AI-driven capex, funding the expansion of data centres, energy infrastructure and grid capacity.

Convertible issuance also tends to re-emerge in periods where equity values are depressed. In addition to tech, another key driver of 2025 and 2026 issuance has been the refinancing of convertibles issued during the pandemic (convertible bonds tend to have a 5-year term).

Why convertibles? The issuer’s perspective

- Cheaper than vanilla bonds: In the same way as vanilla bonds, convertibles require regular coupon payments, but a key attraction for issuers is that the coupon on convertibles offers a saving over other sources of debt. The equity conversion right offers value to investors that compresses the coupon, which is why convertibles tend to come to the fore when funding rates are heightened.

The price differential between conventional bonds and convertible bonds depends on the issuer. Savings of around 200bps p.a.[4] might be viewed as typical, although in some cases differentials can be significantly more dramatic.

|

In the US, CoreWeave, the AI cloud computing company, recently issued a convertible at 1.75% on the same day it priced a traditional secured bond at approximately 10%.[5] |

- Swift access to funding: Timetables for convertible issuance are generally short and sharp – with proper preparation and engagement. Light touch disclosure requirements allow for a significantly shorter period of preparation than would be the case for a standalone vanilla issuance.

- Equity issuance at a premium: Convertibles can offer advantages compared to a rights issue or other form of equity issuance. The conversion price is set at a premium. The amount varies but is typically around 25-30% over the prevailing share price. This premium may offer economic benefits when weighed up against a rights issue (where shares are typically offered at a discount).

- No immediate dilutive impact: Convertibles defer the dilutive impact of issuance on existing shareholders, which may be perceived as another advantage when compared to a straight equity issue. Convertibles may even be structured to minimise dilution impact on conversion if that is a concern, through the use of cash settlement and other options, subject to tax considerations.

- Diversification and gearing: Other benefits of convertibles for issuers include funding diversification (they open up the issuer’s debt stack to equity-linked investors). Although not guaranteed, improvements to the balance sheet if the equity performs well may be another driver. On conversion, the bond – and therefore the debt component - is extinguished.

Legal and documentation considerations

It can be a surprise to some issuers that the process of issuing convertibles can be simpler than straight debt or equity, in particular in terms of disclosure.

Convertibles are settled through the clearing systems in the normal way, but are usually listed on an exchange-regulated market rather than a Prospectus Regulation venue. A popular choice for listing convertible bonds is the Open Market (or Freiverkehr) segment of the Frankfurt Stock Exchange.

This means that listing particulars can be prepared under the relevant MTF’s rules. These are lighter, faster and less costly than a full prospectus, and can be avoided altogether for issuers with shares admitted to an EEA or the UK regulated market.

The terms and conditions of the bond are not materially different from a Eurobond (for example the negative pledge and Events of Default). Due to the need to cater for the conversion option and related protections, certain aspects of the documentation are more complicated than a vanilla bond (see further below), but these mechanics are well understood and therefore highly precedent driven.

US Securities Act requirements will have to be considered as in relation to any bond issuance, and there are some specific requirements that may be engaged in the context of convertibles. The complexity of the analysis varies, the key being to ensure it is addressed at the planning stage.

Conversion and adjustment

Authorities to issue shares and pre-emption rights are a key due diligence item for issuers considering a convertible. However, if this cannot be addressed prior to issuance, there are various techniques that are employed.

For example, for UK plcs the typical work-around is a “Jersey cashbox” structure. This involves the convertibles being issued by a Jersey-incorporated finance subsidiary of the listed parent (the cashbox). On conversion, the investors receive preference shares from the Jersey cashbox, which they can exchange with the listed parent for ordinary shares (making use of the Companies Act 2006 exemption from pre-emption rights for issues of equity shares for non-cash consideration).

The terms and conditions will make provision for adjustments to the conversion price to ensure bondholders are not adversely impacted by changes to the equity structure of the issuer. Adjustment events will include, for example, consolidation or sub-divisions of the ordinary shares, modifications to shareholder rights, new issuance, buybacks and dividends and any change of control/de-listing.

These provisions (and the adjustment formulae) are dense and complex but, as noted above, well understood.

ConvEx, or another specialist calculation agent, will be appointed to manage the conversion and adjustment calculations.

Pricing and share price volatility

As noted above, issuing a convertible bond can diversify a company’s debt stack through the allocation of bonds to existing long-only investors, as well as to multi-strategy investors.

These multi-strategy investors typically hedge their equity exposure in respect of the convertible bond by shorting the issuer’s stock, which can result in volatility in the share price around the time of issuance. One practice which has evolved to try and address this is the use of a delta placement to set a “base price” for the issuer’s shares, to which a premium is then applied in order to set the conversion price.

A delta placement is an accelerated bookbuild, using existing shares in the issuer, which is carried out after market close by the banks at the time of launching the transaction.

The delta placement is intended to provide investors with access to shares for the purposes of their hedging activities and to minimise the potential share price disruption which can arise if a number of investors independently enter the market for hedging purposes. However, the use of a delta placement to set the “base” share price is not universal and the advice of the banks on optimising execution of the bond will be important.

Careful thought from an investor relations perspective may also be needed and an issuer may wish to agree with their banks certain review and consultation rights in relation to the initial allocations and, in particular, the proportionate allocations to long-only and multi-strategy investors.

Tax, accounting and balancing the economics

In practice, the main complexities of convertible issuance lie in getting the economics right, which includes the accounting and tax treatment.

Embedding an equity option within a debt instrument can give rise to issues with coupon deductibility, tax grouping (if the issuer is not the group parent) and transfer taxes, as well as questions as to how any profit or loss on the embedded option should be treated for tax purposes for the issuer. However, in many jurisdictions, with careful structuring it is usually possible to achieve coupon deductibility and to avoid any material adverse tax consequences.

For example, for a UK issuer, provided the convertible bond is listed, convertible into shares in the group parent where the issuer is a subsidiary and trades settle within a clearance system, the coupon would usually be deductible and any profit or loss arising to the issuer on the embedded option would be non-taxable. Further, the convertible should trade free of stamp duty.

Comment

A number of factors - the growth trajectory of the AI sector, the recent uptick in IPOs (within and outside tech), ongoing geopolitical fragility and the global battle against inflation and related pressure on interest rates - might suggest that the current wave of convertibles issuance could have more longevity than in previous cycles. There is also evidence of interest among a broader range of sectors, including names in tech, industrials, defence, energy and retail.

Will convertibles take on more permanence as part of the funding toolkit? We suspect the drivers for issuance will remain heavily context specific - the treasurer’s “friend for a reason” and “friend for a season” but, not necessarily, “friend for life”.

This material is provided for general information only. It does not constitute legal or other professional advice.