FRC PUBLISHES ANNUAL REVIEW OF CORPORATE REPORTING 2024/25

On 30 September 2025, the FRC published its Annual Review of Corporate Reporting 2024/25, outlining findings from its review of 222 annual reports (FTSE 350, AIM, and large private companies) during the year ending 31 March 2025 (FRC Press Release). The review highlights areas for improvement and sets expectations for the next reporting season.

Key findings

- Overall reporting quality among the reviewed FTSE 350 companies was maintained. However, there is a continuing quality gap between FTSE 350 and other companies; most restatements arose outside the FTSE 350. A thematic review of 20 smaller listed and AIM companies is ongoing and a report on this will follow later this year.

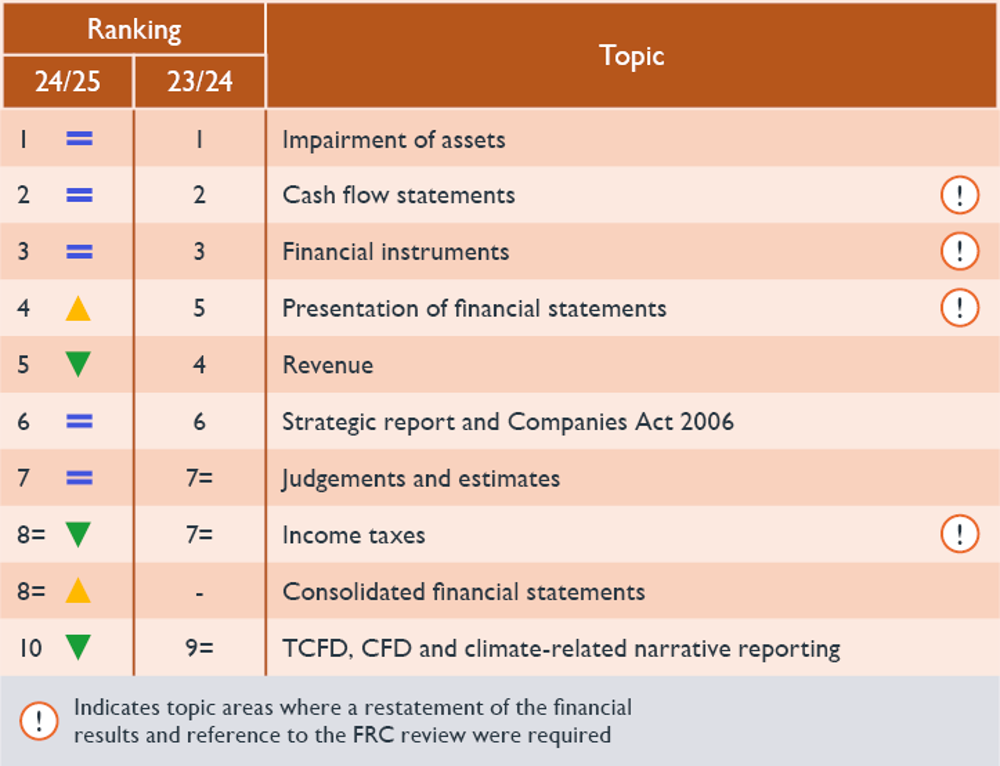

- Impairment of assets remained the most common issue. Clearer disclosures and better cross-referencing would have reduced queries.

- Cash flow statements generated the second-highest number of queries, mainly due to classification errors outside the FTSE 350.

- Inconsistencies between the financial statements and other report sections remain a significant trigger for queries.

- Explanations of significant judgements and estimates require improvement; geopolitical and economic risks increase uncertainty in estimates.

- There were fewer substantive questions on Task Force on Climate-Related Financial Disclosures (TCFD) reporting, which is in its third year for most listed companies.

Expectations for 2025/26 reporting

- Ensure coherent, clear, concise disclosures of all material and relevant information. Does the annual report and accounts as a whole tell a consistent and coherent story throughout the narrative reporting and financial statements? Include only material and relevant information – good quality reporting does not necessarily require a greater volume of disclosure

- Operate robust pre-issuance review processes to identify common technical compliance issues. Many questions and corrections could be avoided by reviewing against the top ten issues (opposite), including ensuring that clear, company-specific accounting policies are included for key matters such as revenue recognition.

- Provide clear, consistent disclosures on judgements, uncertainty and risk. These must be sufficient for users to understand the positions taken in the financial statements. The FRC frequently asks companies to enhance their disclosures when they fail to comply with requirements in these areas.

- Present a strategic report that is fair, balanced and comprehensive on current position and future prospects. Take care to comply with the applicable climate-related reporting requirements, ensuring disclosures are concise and that material information is not obscured.

Top ten areas for substantive queries

DIGITISATION OF SHAREHOLDINGS: THE ROAD AHEAD

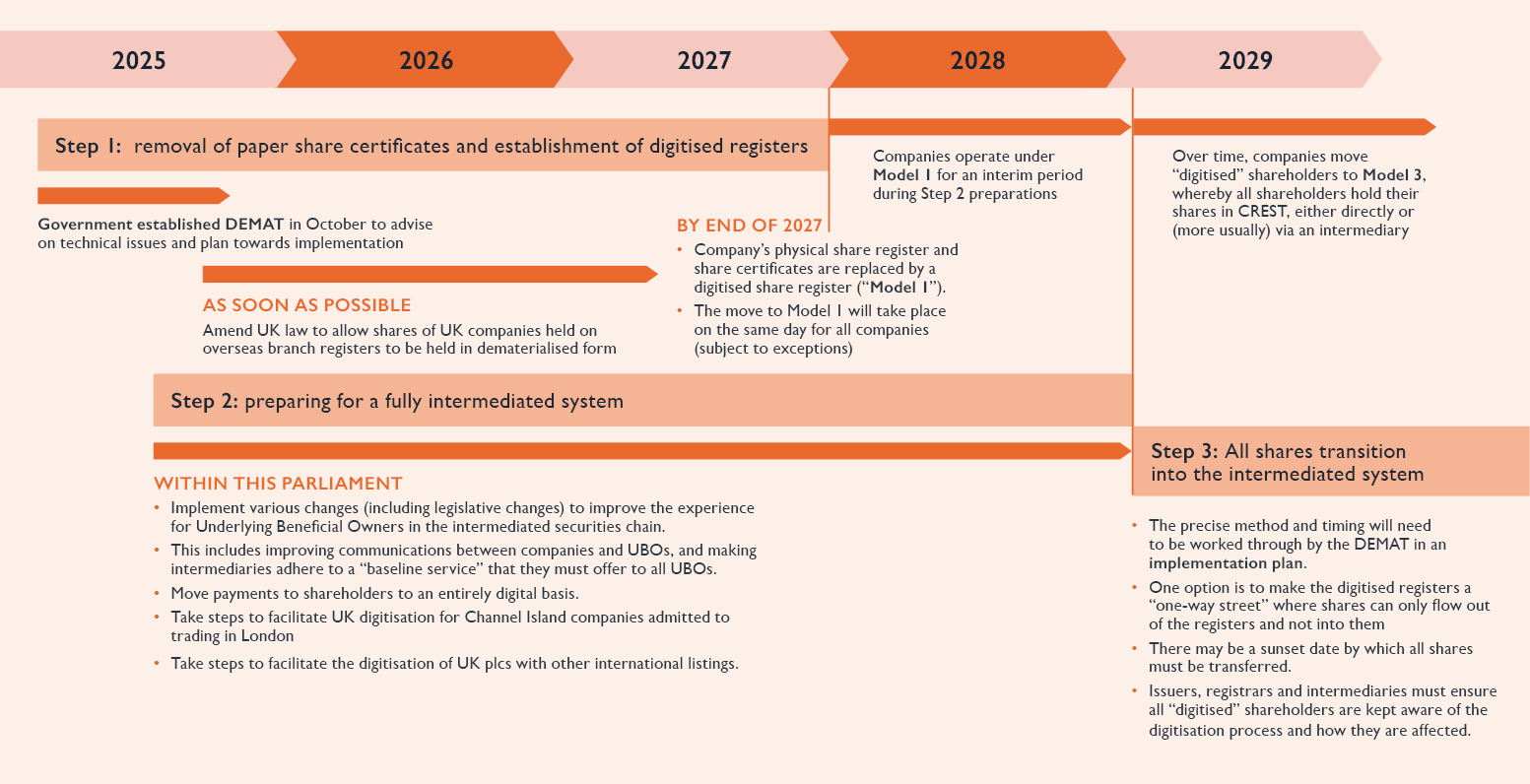

In July, the Digitisation Taskforce, led by Sir Douglas Flint, delivered its Final Report setting out its recommendations for modernising the UK’s share ownership framework in public companies. The government has accepted all the recommendations and in October it established the Dematerialisation Market Action Taskforce (DEMAT), to advise on technical issues and finalise the details for implementation.

The implementation of the proposals set out in the report is seen as important in modernising the UK’s financial markets, enhancing competitiveness with other markets that are already embracing full digitisation, and delivering growth in alignment with the government’s broader capital markets agenda.

The Taskforce has set out a three-step process towards full digitisation. This staggered approach has mainly been adopted to allow time for improvements to be made to the intermediated securities chain and ensure a baseline set of rights that underlying beneficial owners (“UBOs”) will continue to be able to exercise when they cease to be direct shareholders and transition to a fully intermediated system, as well to address certain other legal and other issues. Note that the recommendations are relevant for listed public companies only; the Taskforce recognised that for private companies, the proposals would not be cost-effective.

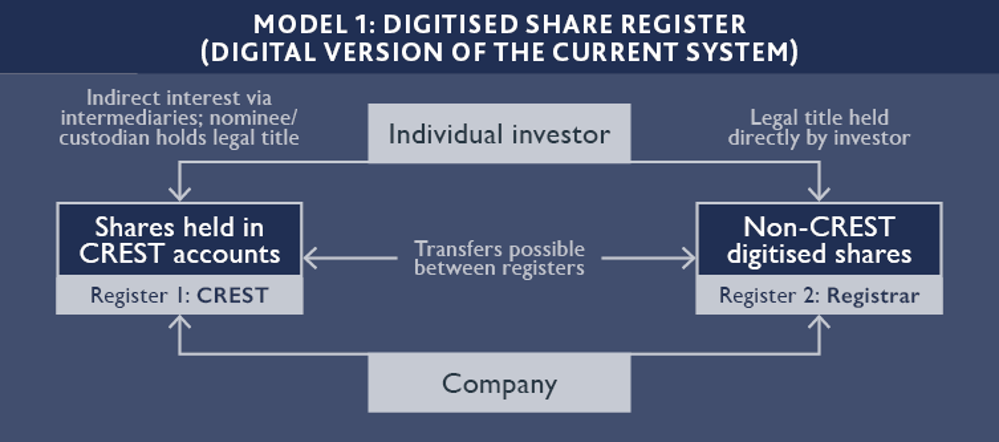

Step 1: Removal of paper shares and establishment of digitised registers

By the end of 2027, current paper share registers and share certificates will be replaced by digitised registers, replicating the service paper shareholders receive today but in digital form (what the Taskforce calls “Model 1”). Share certificates are nullified.

Step 2: Preparing for a fully intermediated system

Companies will operate under Model 1 for an interim period while improvements to the intermediated securities chains and other legislative changes are made. The Taskforce recommends that Step 2 preparations be completed by the end of the current Parliament in 2029.

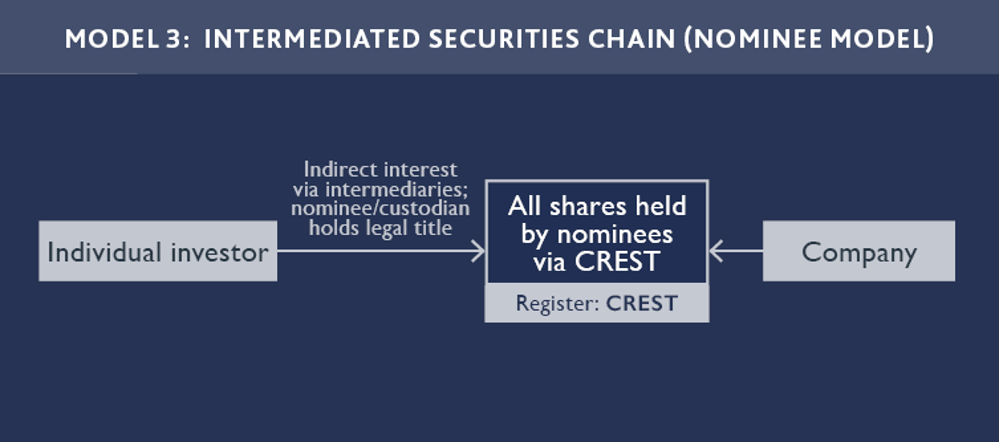

Step 3: All shares transition into the intermediated system

Companies will move all shareholders to a fully intermediated system (“Model 3”). Given that the Step 2 improvements will need time to implement, there is no definitive timeframe yet and DEMAT will prepare an implementation plan in due course. The move from Model 1 will likely be gradual and may involve making the digitised register a one-way street, so shares can only be transferred out of it, but not into it.

Taskforce's indicative timeline for implementing the final recommendations

(Click image above to view)

Why not move to Model 3 at once?

Although adopting Model 3 is the ultimate endpoint, companies will operate under Model 1 for an interim period. This staged approach has been taken principally because improvements are needed to the intermediated system before all shares can be transferred into it, to ensure that ultimate beneficial holders of shares can exercise their rights.

Current intermediated models can give rise to difficulties and delays in communicating information up and down the chain to the investor, or may not allow investors to determine how voting and other rights should be exercised. The Taskforce has made various recommendations to enhance the rights of ultimate investors to address these concerns and proposed a “Bill of Rights” (see box) that will act as a baseline service that intermediaries must offer all shareholders.

Respondents to the consultation also expressed concern about the disruption and costs involved in moving directly to Model 3.

In addition, there are particular issues for certain companies that need to be addressed before moving to Model 3. For a number of companies with overseas listings, Model 3 would be currently unworkable (notably companies with listings of shares in the US and Hong Kong) - for a mixture of legal, operational, regulatory and tax reasons.

Furthermore, there are particular issues for companies with overseas branch registers, notably in Hong Kong (including HSBC, Standard Chartered and Prudential). Improvements need to be made to the inter-operability of international settlement systems before moving to Model 3. The final move to Model 3 may be subject to a small number of exceptions for such companies if interoperability between central securities depositaries has not improved.

What does this mean for listed companies?

The proposals will largely be welcomed by listed companies. The current paper-based processes for issuing certificates and making payments, and for sending documents to shareholders who have opted to receive hard copies, lead to inefficiencies and costs. These costs are effectively subsidised by other investors.

The move away from two registers – a CREST register for dematerialised shares and a register for shares that are held in certificated (paper) form – to one single CREST register will also bring savings in the long run, although there will be an interim period where the company will continue to maintain two registers.

Companies will need to work with their registrars to put in place the necessary arrangements for converting the paper share register to a digitised register under Model 1. It is likely that any legislative changes to implement the proposals will be drafted so as to ensure that companies will not have to amend their articles of association in order to take advantage of the reforms. However, in due course, companies should consider updating them as a matter of good housekeeping.

Crucially, companies and registrars will also need to keep certificated shareholders informed about the changes. Some of the changes – including mandating shareholders to move to an intermediated system for which they will have to pay a fee (as opposed to the “free” service they receive as certificated shareholders) and moving all shareholders to electronic payments – raise PR implications that will need to be handled carefully, especially as certificated shareholders are proportionately more likely to be older.

|

The “Bill of Shareholder Rights” This sets out the Taskforce’s conditions that an intermediary’s baseline service to shareholders (including UBOs) must meet in order for it to be concluded that they are able to exercise their rights effectively and efficiently in the improved intermediated securities chain. |

|

|

1. Right to Receive Company Information Shareholders should be entitled to receive all relevant company information electronically, with the option to receive physical copies where necessary. |

4. Right to Transparent Fee Disclosure Shareholders should be informed of any intermediary fees related to identification, information transmission, and facilitation of shareholder rights. Fees should be non-discriminatory and proportionate to actual costs. |

|

2. Right to Transmission of Information through Intermediaries There should be prompt communication of company information through the intermediated securities chain to shareholders. Intermediaries should be obliged to transmit information about the identity of shareholders to the company, enhancing communication channels between the company and its intermediated shareholders. |

5. Right to Receive Payments Electronically Shareholders should receive payments electronically unless otherwise agreed with the company. |

|

3. Right to Participate and Vote Shareholders should have the right to participate and vote in general meetings, either directly or through intermediaries. They should be entitled to confirmation of vote receipt and assurance of valid recording and counting by the company. Shareholders should also have the right to know that their responses and instructions are transmitted by intermediaries back to the company without delay. |

6. Right to Seek Compensation for Misleading Public Information Shareholders should be able to seek compensation if they suffer a loss due to misleading statements, dishonest omissions, or dishonest delays in the publication of information related to publicly traded securities. |

If you would like more information on any of the matters covered, please do contact us, or speak to your usual Slaughter and May contact.

This material is provided for general information only. It does not constitute legal or other professional advice.