Shareholder activism update

Shareholder activism remains firmly on the corporate agenda, as global campaign volumes hold strong. In this piece we look at current activism trends and examine some recent high-profile European campaigns.

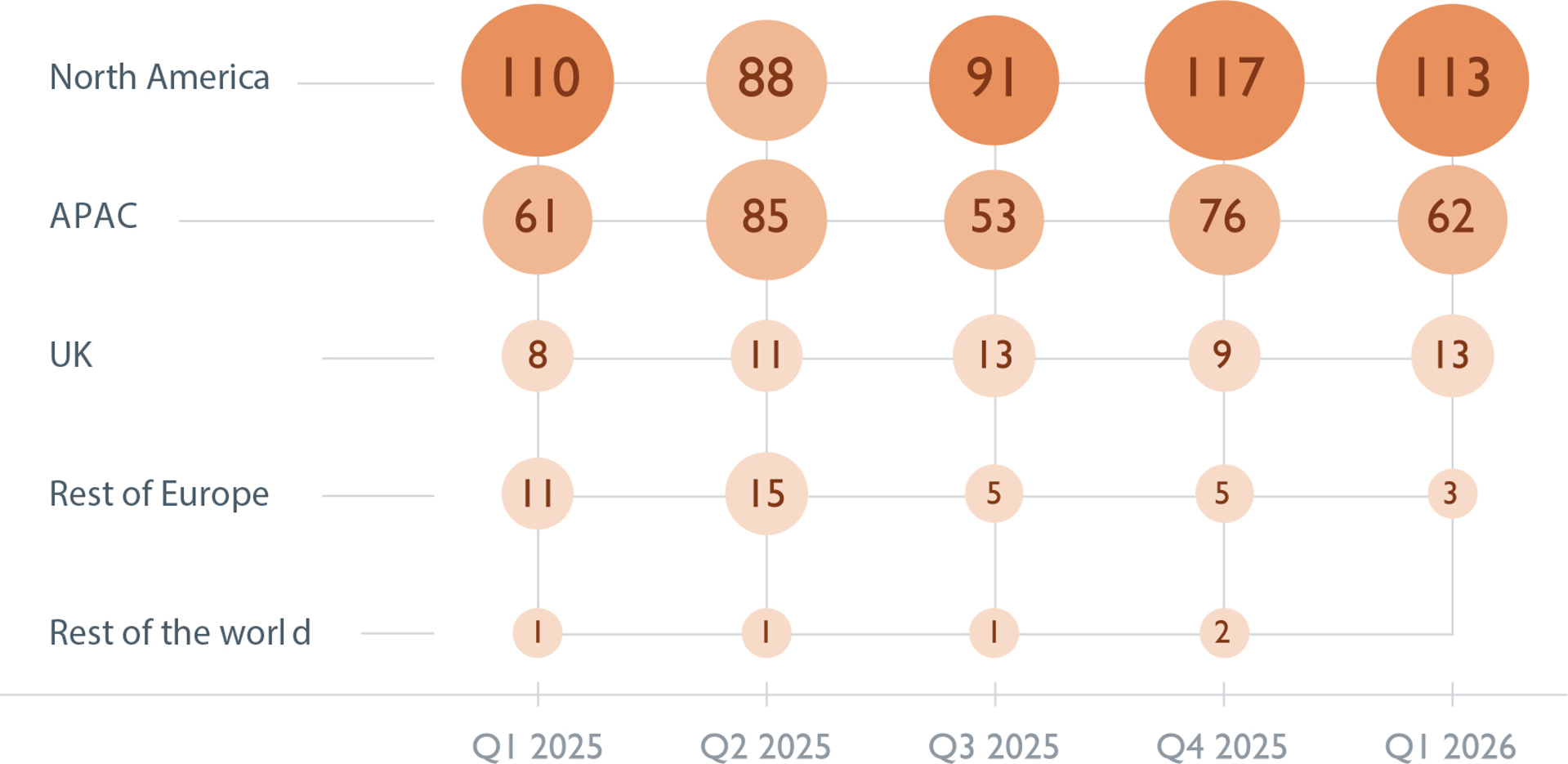

The US and Japan (which accounted for 93% and 80% of the campaigns recorded in the North America and APAC regions respectively) together dominated global activism activity. Europe saw another busy quarter sustaining the momentum seen in the second half of 2025 with activity focused on UK

listed companies which were targeted in 13 of the 16 public campaigns in Europe.

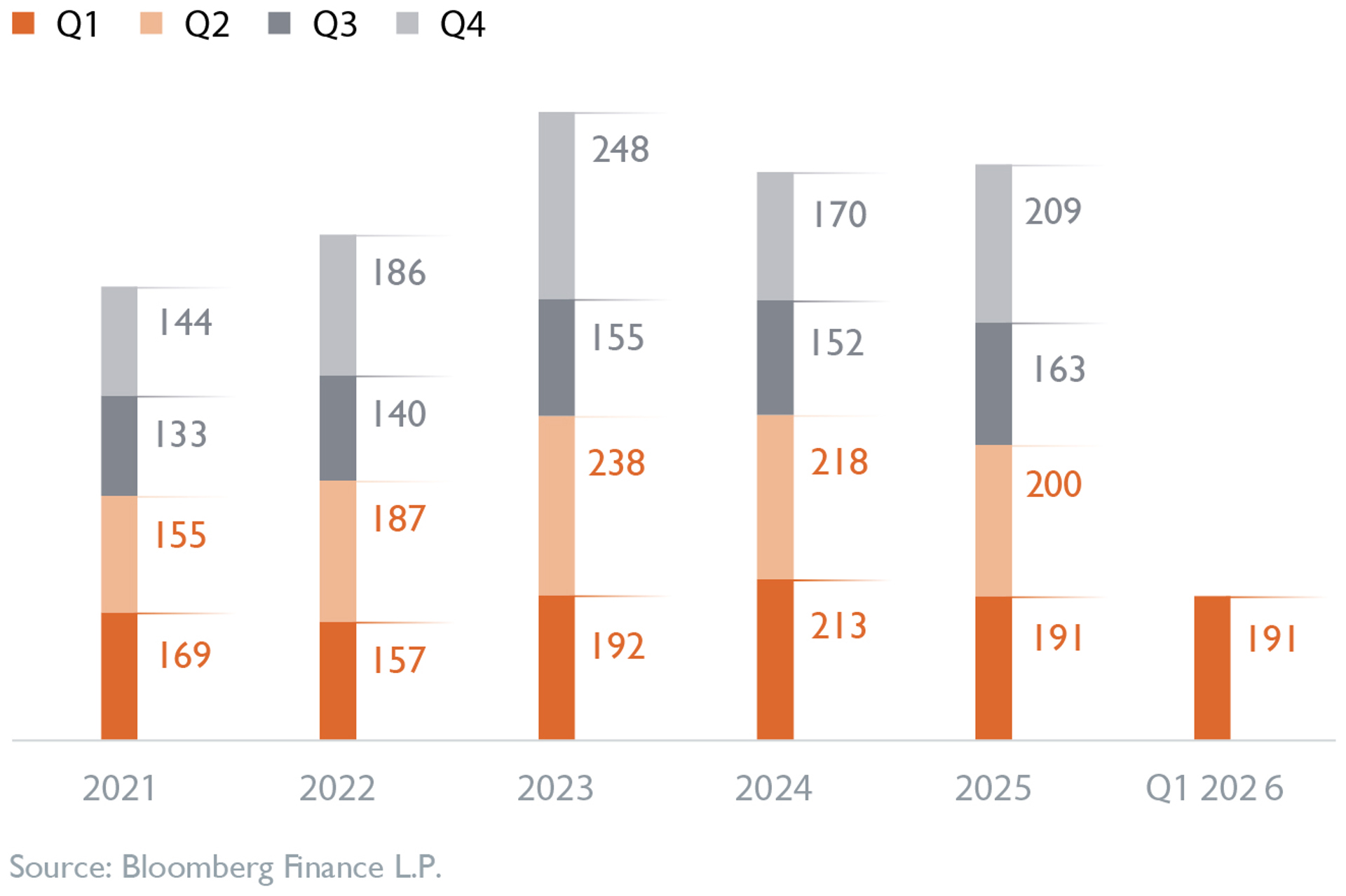

Number of campaigns globally

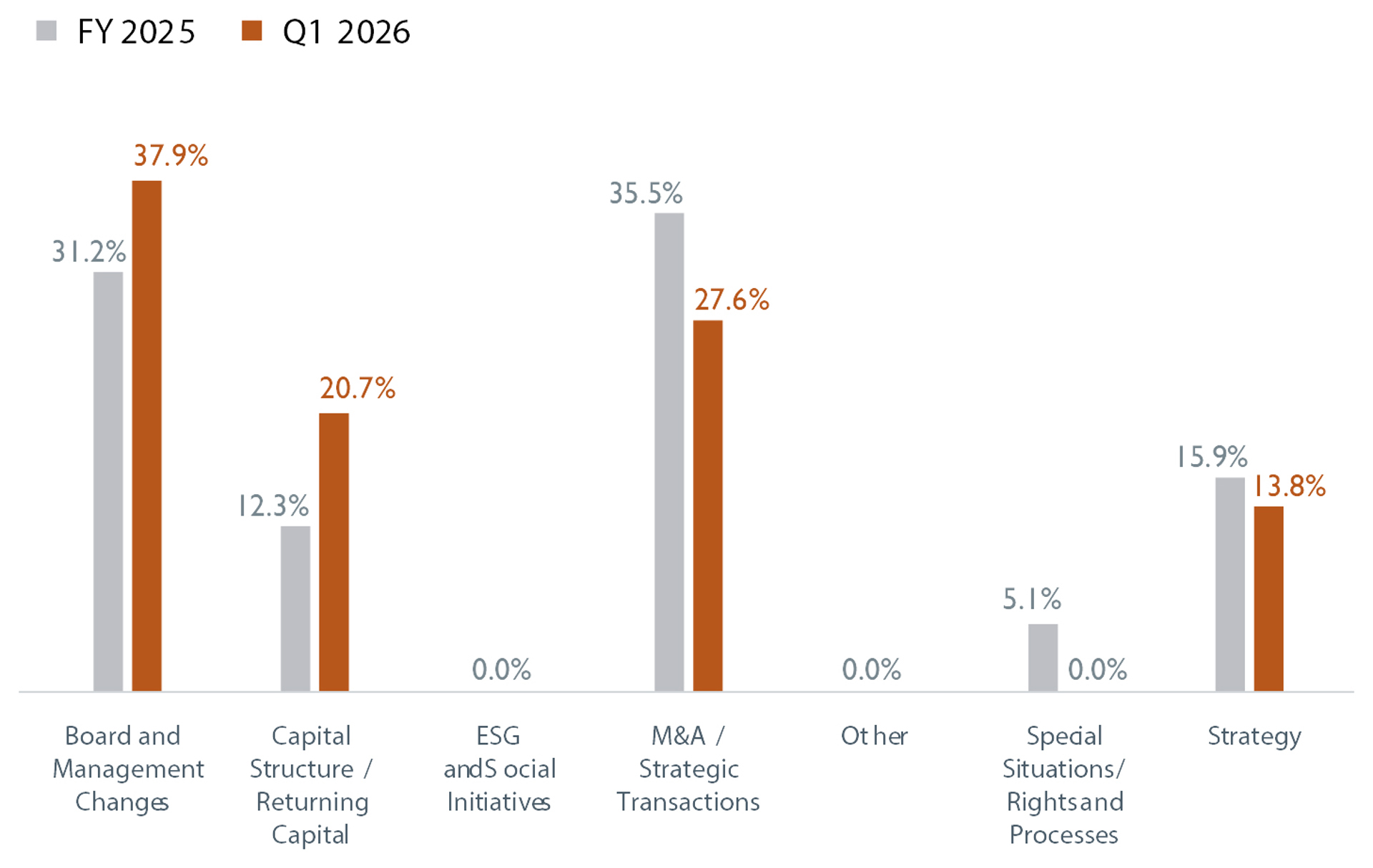

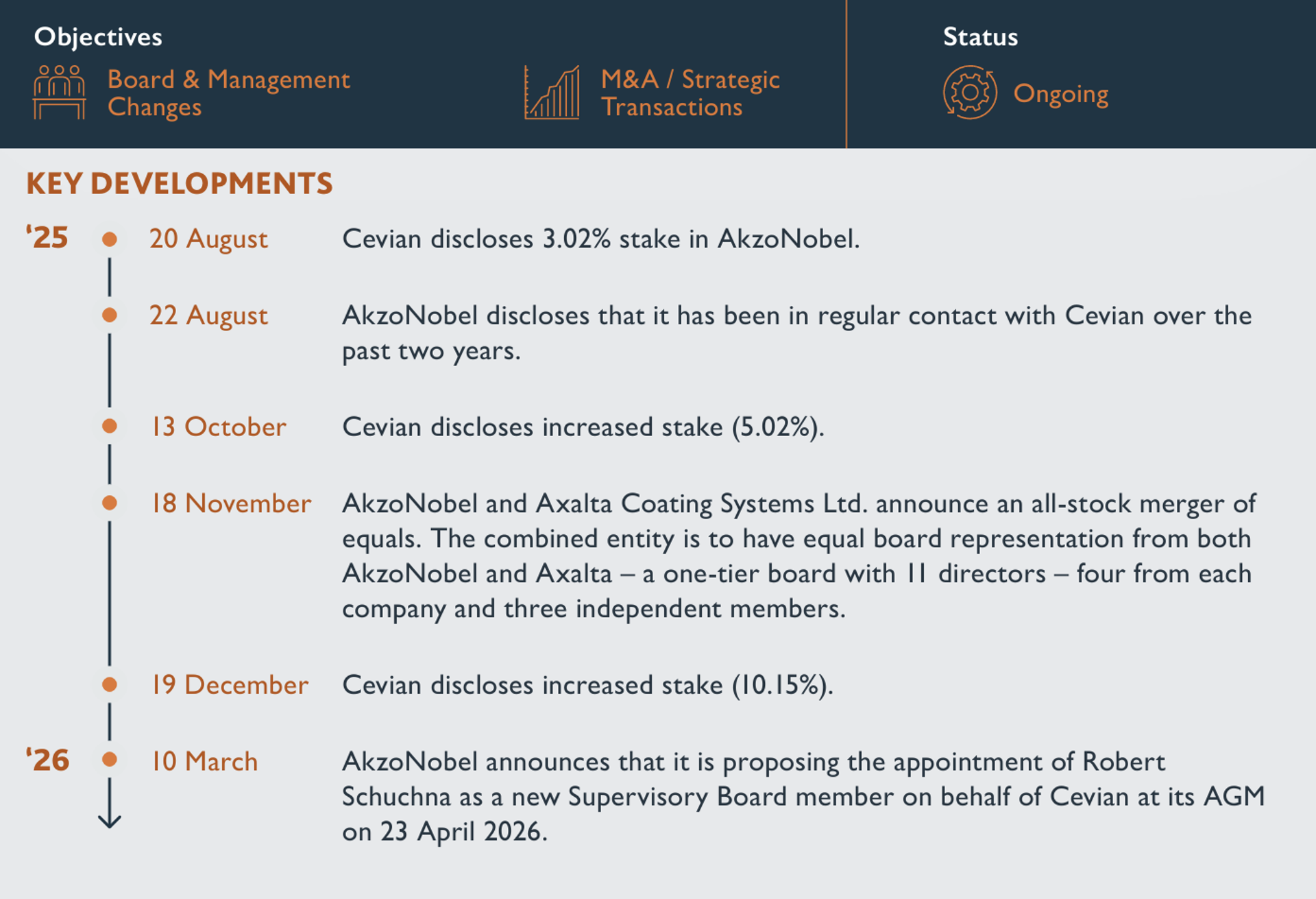

Board and management changes remain the leading campaign objective globally (43% of campaigns) often alongside a broader agenda. Activists achieved representation on the boards of 39 targets globally in the first quarter, already over a third of the full-year total for 2025, 22 with the proposed appointment of a Cevian nominated representative to AkzoNobel’s Supervisory Board thought to be a first in the Dutch market. Activists have maintained their focus on M&A, with M&A related demands appearing on the agenda of 27% of global campaigns playing out.

Number of campaigns by region

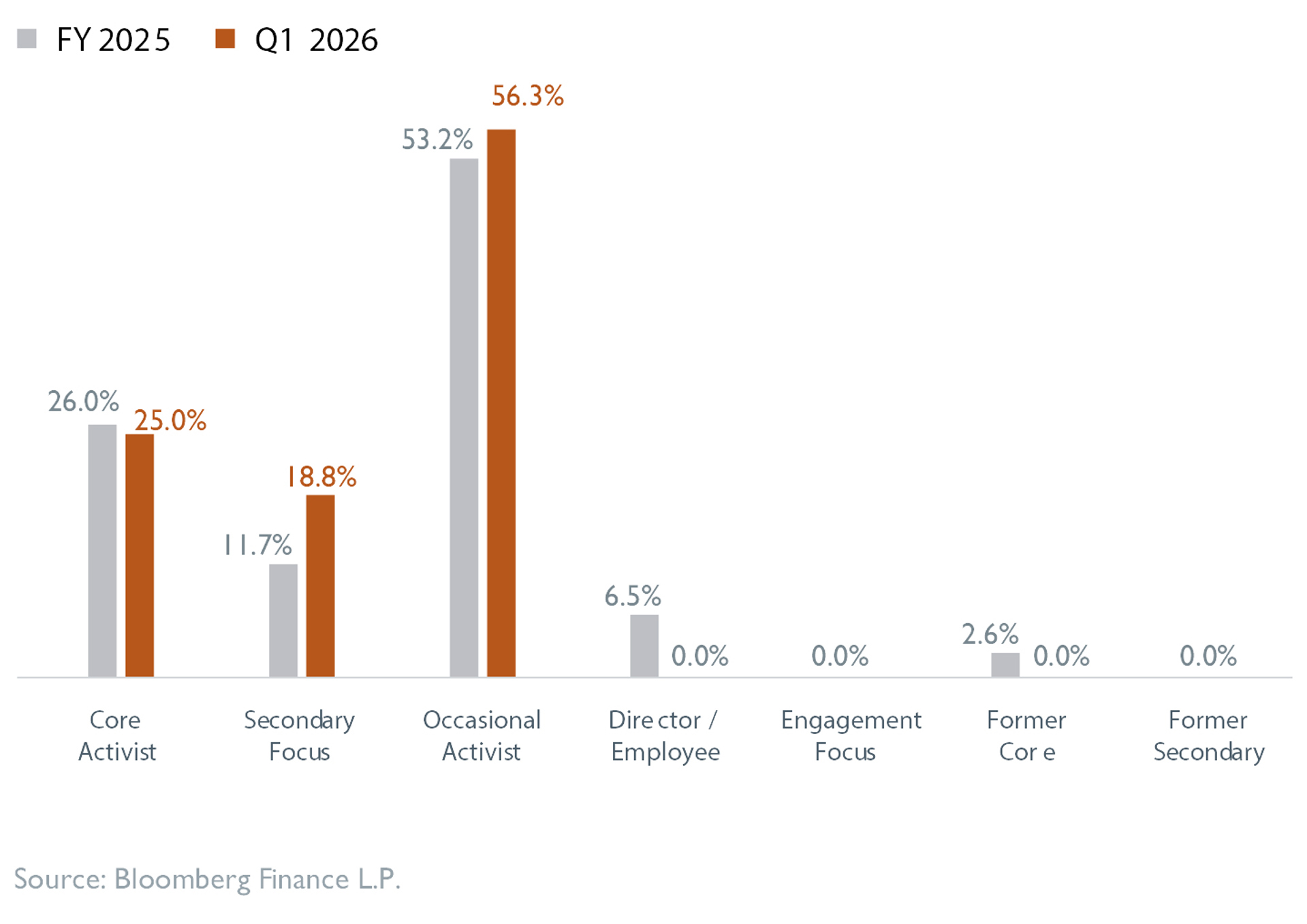

Although traditional activist investors wage the highest number of campaigns globally, the number of campaigns by occasional activists is almost on equal footing. A history of successful campaigns is no longer a prerequisite to win support from proxy advisers and institutional investors. AI is unsurprisingly reshaping the activist landscape, facilitating occasional activists in spotting opportunities, and building theses on potential targets – raising the bar for target preparedness and campaign defence.

UK campaigns dominate European activism as board changes and M&A objectives feature high on the agenda

The UK, which is consistently the busiest market in Europe for activist activity, saw an outsized share of European activity as public campaign numbers dipped in continental Europe whilst remaining robust in the UK. Activism preparedness remains a priority for UK listed corporates, as the data reveals only part of the story – for each public situation, multiple campaigns are initiated and, in most cases, remain behind closed doors.

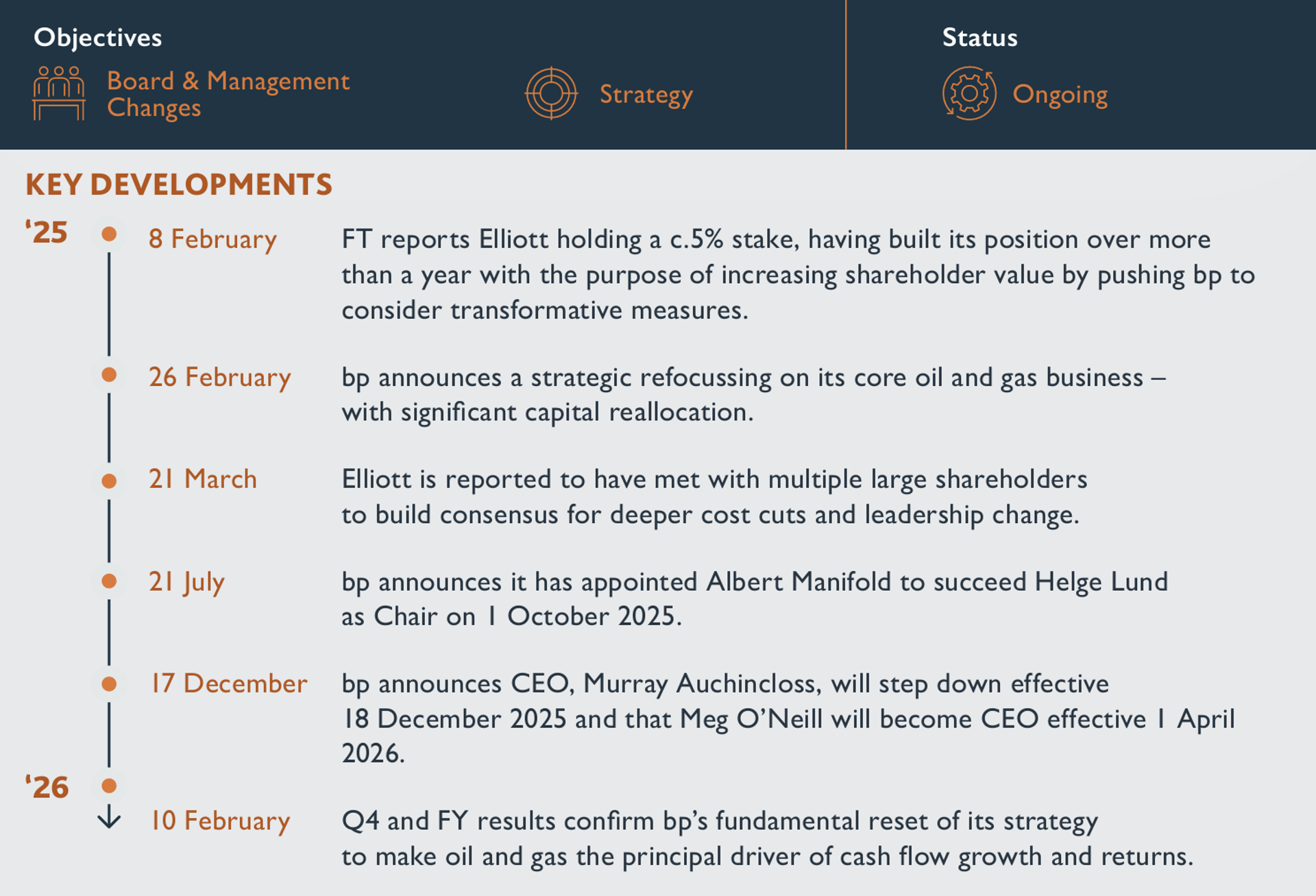

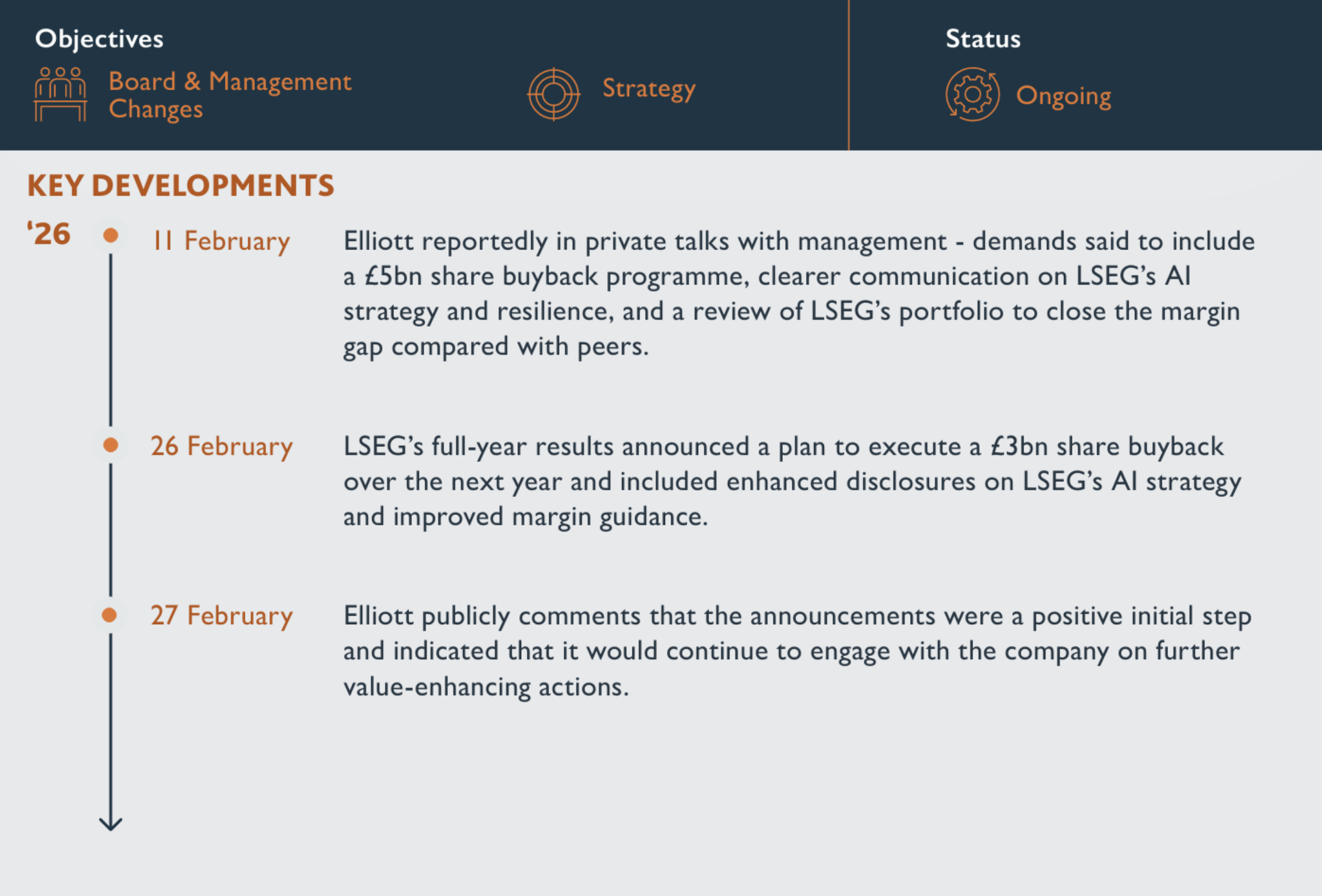

The leading US-based activist funds remain the cornerstone of the current European activism landscape and have been responsible for the most prominent recent UK campaigns – including Elliott’s positions in bp and the London Stock Exchange Group and Saba Capital’s interventions at various UK investment trusts.

Activist type in Europe

Demand for board and management changes continues to be the leading objective in UK activism campaigns – with board representation demands on the agenda of 8 of the 13 UK campaigns that started this quarter. M&A objectives, together with demands for a strategic review or break-up, feature prominently – together appearing on the agenda in 41% of European campaigns.

Capital structure and capital returns objectives were also on the agenda – cited 6 times across the 13 UK campaigns – signalling growing activist pressure on UK boards to sharpen their capital allocation discipline in the context of an ongoing challenging macro-economic environment.

European campaign objectives

bp faces countervailing shareholder pressures from Elliott and climate activists

- Follow This, a Dutch non-profit activist investor, has been critical of bp’s strategic pivot back towards hydrocarbons and the associated reduction in green energy investment – linking the turnaround to pressure from Elliott.

- In January 2026, Follow This stated that it, together with a group of institutional investors, had submitted shareholder resolutions requiring bp to publish a report on its strategy, investments, production forecasts and cash flows for scenarios of declining demand for fossil fuels.

- 6 March 2026: bp’s AGM notice does not contain a resolution requisitioned by Follow This. A similar climate resolution filed by the Australasian Centre for Corporate Responsibility does appear on bp’s AGM agenda. bp has recommended that shareholders vote against it.

- 25 March 2026: Following bp’s decision not to table the resolution at its AGM, scheduled for 23 April 2026, Follow This reportedly issues a letter before action, giving bp until 1 April to respond.

- 23 April 2026: shareholders reject two resolutions at bp’s AGM – a resolution to permit wholly virtual meetings and a resolution to revoke two historic shareholder resolutions mandating bp to make certain climate change disclosures.

Elliott reportedly seeks to smooth political sensitivity

- Elliott’s shareholding in London Stock Exchange Group (LSEG) has reportedly prompted concern within the UK Treasury given the importance of LSEG’s role in the UK’s capital markets.

- The UK government was alleged to be concerned that Elliott’s demands could include a break-up of LSEG or a re-listing in the US.

- Elliott has reportedly proactively engaged with UK Treasury officials to address those concerns.

A landmark activist driven board appointment for the Dutch market

- Activist-driven director appointments are structurally very challenging in the Netherlands. In the Netherlands, director appointments are tabled to the AGM via a board nomination. There is typically no opportuity for an activist to place a rival candidate on the same agenda in competition with the board’s nominee – the only option is to vote the board’s candidate down.

- Schuchna’s proposed appointment to AkzoNobel’s Supervisory Board, achieved by persuading the company to table the nomination itself, is thought to be a first in the Dutch market – but consistent with Cevian’s typical approach.

- Cevian has achieved representation on the boards and/or nominating committees of c. 75% of all its disclosed portfolio companies since its founding in 2002 (although the percentage is significantly lower when looking at Cevian’s investments in UK listed companies).

If you would like more information on any of the matters covered, please do contact us, or speak to your usual Slaughter and May contact.

This material is provided for general information only. It does not constitute legal or other professional advice.